As a landlord or property manager, you know how important it is to stay on top of every expense. Maintenance costs, repairs, and utilities are usually tracked, but bank fees for checking accounts are often overlooked. These charges can add up, but there are ways to avoid them altogether.

This guide walks you through the most common checking account fees and provides a list of the best no-fee checking accounts for landlords, plus tips on how to choose the right one for your rentals.

Key takeaways

- Traditional business checking accounts often require high minimum balances, typically between $500 and $15,000, to avoid monthly fees.

- Per-transaction fees can add up fast. Many banks limit free transactions to 100–250 per month, charging around $0.25 to $0.75 per excess transaction.

- No-fee bank accounts eliminate maintenance fees and transaction charges, helping you save up to $3,000+ per year, depending on portfolio size.

- The best no-fee options offer unlimited transactions, zero minimums, free ACH transfers, and landlord-specific features like rent collection and bookkeeping tools.

- Only use no-fee bank accounts insured by the FDIC or NCUA for coverage up to $250,000 or more.

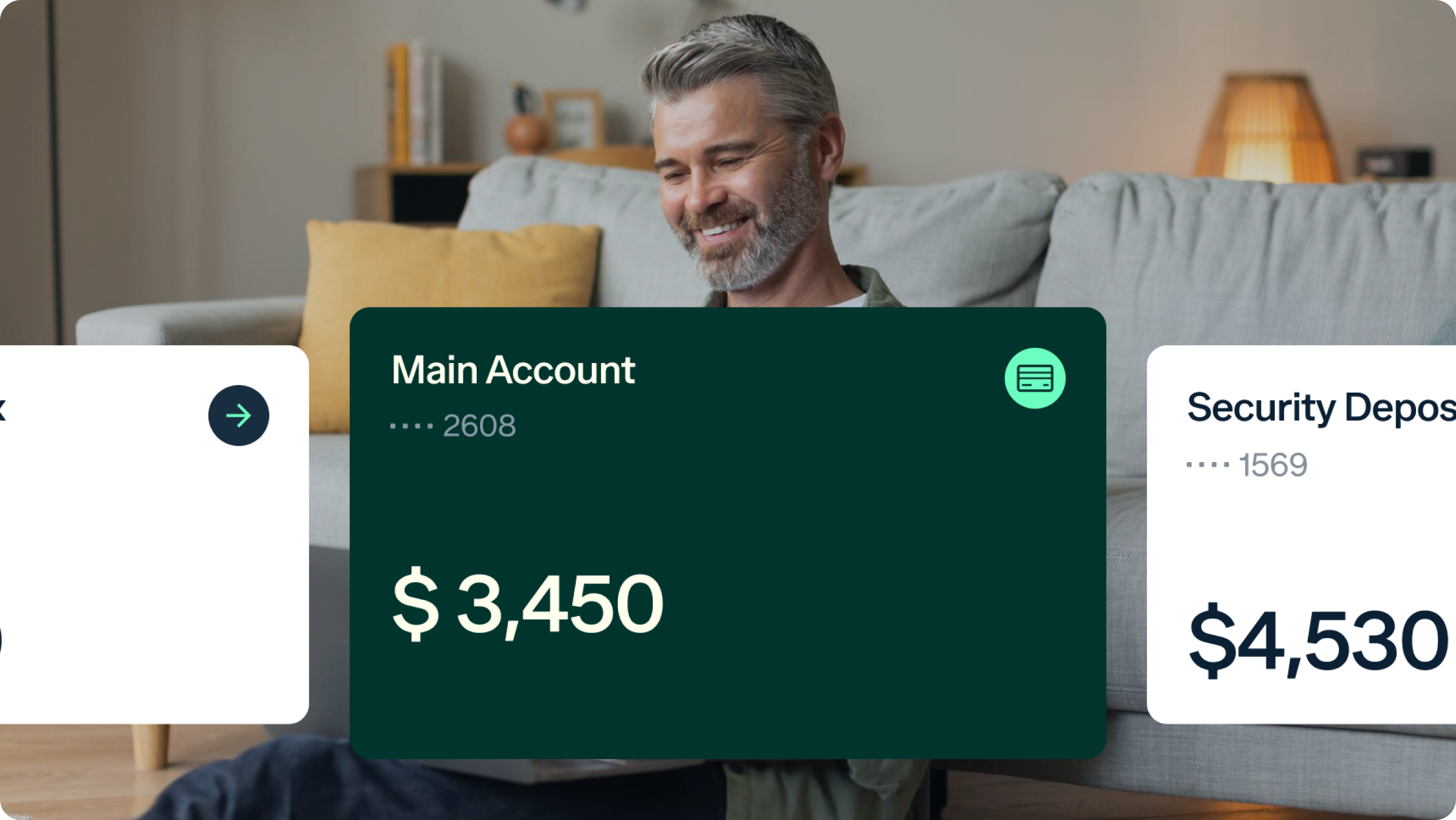

Open unlimited accounts for properties and security deposits with no monthly fees.

Why no-fee banking is essential for landlords

Banking fees can silently drain thousands of dollars from businesses annually. Choosing a landlord-friendly bank account that offers no monthly fees, no minimum balances, and smart financial tools can make a big difference.

We’ve broken down the most common checking account fees traditional banks charge below.

Monthly account maintenance fees by traditional banks

Traditional banks often charge monthly maintenance fees just to keep your account open. These fees apply whether or not you’re actively using the account and can quickly add up, especially if you manage multiple properties or entities.

Here’s a summary of traditional bank fee structures and their impact on small, medium, and large portfolios:

How much landlords really pay in bank fees

| Portfolio Size | Units Managed | Typical Bank Account Setup | Avg Monthly Fee Per Account | Est. Monthly Cost | Est. Annual Cost |

|---|---|---|---|---|---|

| Small | 1–5 units | 1–2 personal or business checking accounts | $10–$95 | $10–$190 | $120-$2,280 |

| Medium | 6–20 units | 2–5 business checking accounts | $10–$95 | $20–$475 | $240–$5,700 |

| Large | 20+ units | 5–10+ accounts | $10–$95 | $50–$950+ | $600–$11,400+ |

Example: A medium-scale landlord with four LLCs and 12 rental units uses four business checking accounts at a traditional bank. Each account charges a $15 monthly fee, totaling $60 per month just to keep the accounts open.

If two accounts dip below minimums due to renovation expenses or vacancies, that’s $30 in fees for the month, or $360 annually, just for not meeting balance requirements.

Fees for dropping below minimum balance

Many banks advertise “free” business checking accounts, but only if you maintain a minimum daily or monthly balance, often ranging from $500 to $15,000. A decrease in your balance, common during renovations or tenant turnover, may result in monthly fees.

Typical minimum balance fees at traditional banks

| Bank Type | Avg Monthly Minimum | Avg Monthly Fee |

|---|---|---|

| Basic Business Checking | $500+ | $10–$15/month |

| Business Checking (Mid-Tier) | $2,000+ | $15–$30/month |

| Premium Business Accounts | $15,000+ | $30+/month |

Estimated penalty fees by portfolio size

| Portfolio Size | Typical Setup | Risk Level for Breach | Est. Monthly Penalties | Est. Annual Cost |

|---|---|---|---|---|

| Small (1–5 units) | 1–2 basic accounts, lower balances | High (irregular cash flow) | $10–$30 | $120–$360 |

| Medium (6–20 units) | 2–5 business accounts | Medium (spikes during repairs or vacancies) | $30–$150 | $360–$1,800 |

| Large (20+ units) | 5–10+ premium accounts, multiple LLCs, or reserve allocations | Medium–Low (higher liquidity, but more accounts = more risk) | $150-$300+ | $1,800-$3,600+ |

Per-transaction fees

Most traditional business checking accounts include a limited number of free transactions per month, typically 100 to 250. After that, you pay per transaction, ranging from $0.25 to $0.75 per item.

What counts as a transaction?

Transactions that may incur fees include:

- Rent deposits

- ACH payments to vendors/contractors

- Utility payments

- Property insurance premiums

- Mortgage payments

- Maintenance purchases (via debit card)

- Transfers between accounts

- Reimbursements to partners

- Bank bill pay usage

Estimated transaction volume by portfolio size

| Portfolio Size | Units | Est. Monthly Transactions | Est. Annual Transactions |

|---|---|---|---|

| Small | 1–5 units | 20–50 | 240–600 |

| Medium | 6–20 units | 60–150 | 720–1,800 |

| Large | 20+ units | 150–400+ | 1,800–4,800+ |

Estimated excess per-transaction fees (traditional banks)

| Portfolio Size | Bank Type | Free Transactions | Common Fee Over Limit | Est. Monthly Excess Cost | Est. Annual Cost |

|---|---|---|---|---|---|

| Small | Basic Business Checking | 100/month | $0.25 | Usually under limit | $0–$50 |

| Medium | Business Checking (Mid-Tier) | 200/month | $0.50 | $10–$50 | $120–$600 |

| Large | Premium Business Accounts | 250/month | $0.50–$0.75 | $50–$200+ | $600–$2,400+ |

Example: If you’re paying $0.50 per excess transaction, that’s easily $25–$75/month, or $300–$900 per year—for just using your account normally.

Transaction fees will punish you for adding more rentals. The more you scale, the more you’re charged by your bank.

Check out our guide for tips on how to avoid bank fees.

Traditional banks vs. no-fee banking

Traditional banks let you manage your rental property finances, but often come with high fees, minimum balance requirements, and limited flexibility. No-fee banking offers a smarter alternative for landlords, delivering the same core features without the overhead.

The best banks for real estate investors offer no-fee checking accounts, no minimum balance requirements, and built-in property management tools to save even more by not paying for third-party apps.

5 best no-fee/low-fee checking accounts

1. Baselane Banking

Best for: All-in-one banking, rent collection, bookkeeping, and tax reporting in one platform. You can open unlimited free sub-accounts per property and entity, making it easy to separate income, expenses, deposits, and reserves—all under one login.

Key benefits:

- No monthly fees or minimum balance requirements

- Up to 3.35% APY²

- Virtual accounts to separate funds by property

- Virtual debit cards with spend controls

- Recurring payments (ACH, wires, checks) and auto-transfer rules

- 55,000+ fee-free ATMs

- Free online rent collection (ACH, debit, credit)

- Automated expense tracking

- Real-time cash flow insights

- On-demand tax reports

- Up to $3M¹ on funds deposited via Thread Bank; Member FDIC

Baselane also offers tenant screening, digital leases, insurance, financing, and more, so you have everything you need to manage your rentals under one roof.

2. Relay Financial

Best for: Small businesses looking for basic account separation. Relay offers up to 20 checking accounts and 2 savings accounts under one business. Since it’s designed for general business operations, you’ll need third-party plugins or separate apps for rent collection and rental property accounting.

Key benefits:

- No monthly or overdraft fees for basic account

- Multiple accounts (20 checking, 2 savings) and debit cards (up to 50)

- Offers basic bookkeeping

- Integrates with QuickBooks

3. Bluevine Business Banking

Best for: Earning interest on balances and occasional cash-back perks. Bluevine offers up to 20 sub-accounts under a single EIN and pays 1.5% APY on standard plans. Higher APYs are available, but only through paid tiers. It’s not tailored for landlords and lacks property-specific features.

Key benefits:

- Monthly fee of $0 to $95/month

- 1.5% APY (up to 3.7% APY on paid plans)

- Cash back on select purchases

- FDIC insured for up to $3M

4. Novo Business Checking

Best for: Landlords with basic banking needs. Novo is a free online banking platform that offers simple integrations like Stripe and QuickBooks Online. It may suit landlords with a small number of units, but it lacks property-specific tools or features tailored to rental management.

Key benefits:

- No monthly fees, no minimums

- Refunds ATM fees

- Basic expense tracking and budgeting tools

- Integrates with Stripe, PayPal, and QuickBooks

5. Lili Banking

Best for: Sole proprietors managing finances under one EIN. Lili is a digital banking platform with no monthly fees. It offers expense tracking and invoicing, but lacks support for multiple accounts or property-specific tools.

Key benefits:

- Basic plan has no fees, no minimum balance

- Premium plan ($33/month) automatically allocates funds towards tax payments

- Real-time Schedule C tax categorization (not property-specific)

- Free Visa debit card

Compare top low-fee and no-fee business bank account options

If you own a few properties, Bluevine or Novo offer simple setups but lack property-specific tools and require separate logins for each EIN. For landlord-friendly banking, consider platforms like Baselane that support multiple accounts and entities with built-in rental property management tools.

| Feature | Baselane | Relay | Bluevine | Novo | Lili | Local Credit Unions |

|---|---|---|---|---|---|---|

| Monthly Fee | $0 | $0 to $30/month | $0 to $95/month | $0 | $0-$33/month | $2-$16.95/month |

| Security Deposit Accounts | ✔ Compliant | ❌ | ❌ | ❌ | ❌ | ✔ |

| Rent Collection | ✔ Built in | ❌ | ❌ | ❌ | ❌ | ❌ |

| Debit Card | ✔ Spend controls | ✔ | ✔ | ✔ | ✔ | ❌ |

| Open Multiple Accounts | ✔ Unlimited | 20 checking, 2 savings | Up to 20 | ❌ | Up to 4 | Difficult |

| Bookkeeping | ✔ Built in | Basic | ❌ | Basic | Some paid plans | ❌ |

What makes a no-fee bank account ideal for rental property management?

A no-fee bank account is ideal for rental property management because it helps reduce costs, improve cash flow, and simplify operations without sacrificing key features. The best bank account for Airbnb business owners and long-term rentals includes unlimited transactions, free ACH transfers, and the ability to separate funds by property or LLC under one login.

A bank account should also support automated rent collection and expense tracking. Some even include a high-yield savings account to help you earn more on reserve funds.

| Feature | Why it Matters |

|---|---|

| No monthly fees | Keeps fixed costs down, regardless of balance or activity |

| No minimum balance requirement | Flexibility for landlords with seasonal cash flow changes |

| Unlimited transactions | Avoid fees when paying vendors or moving money |

| Free ACH transfers | Essential for paying contractors and collecting rent |

| Free debit card access | Track expenses or issue to staff without extra costs |

| Free online bill pay | Pay mortgage, insurance, or utilities directly |

| Integrated rent collection | Accept one-time and recurring ACH, debit, and credit card payments |

5 tips for choosing a no-fee bank account

Not all no-fee bank accounts online are created equal. While many banks advertise “fee-free” checking, the fine print often tells a different story. The ideal account should eliminate fees, simplify your finances, and seamlessly integrate with your property management.

Here’s what to look for when looking for the best no-fee business checking accounts:

1. Avoid “fee-free” with conditions

While some banks advertise “fee-free” accounts, they often come with strings attached. According to Bankrate’s checking account survey, 45% of non-interest checking accounts waive monthly fees only if customers meet certain conditions, such as maintaining a minimum balance. These requirements can be challenging with variable cash flow, making it essential to look for no-fee accounts without conditional stipulations.

2. Prioritize integration with property management tools

The best no-fee online bank accounts should work with the tools you already use. Look for banks that integrate directly with accounting software or property management platforms. It’s even more efficient when your banking platform has built-in features, eliminating the need for third-party software.

3. Use sub-accounts for property separation

If you manage more than one unit, opening multiple accounts or creating sub-accounts is the best way to keep everything organized. It helps separate operating expenses, security deposits, and reserve funds by property or LLC.

Not many banks offer sub-accounts, and those that do usually require a single EIN, so you’ll need a separate login if you manage more than one business. With Baselane, you can open unlimited checking and savings accounts online for multiple entities, giving each property its own account without added costs.

4. Confirm FDIC insurance

Whether you manage a duplex or a 50-door portfolio, your deposits should be safe. Make sure your bank is FDIC insured, covering balances up to $250,000 per account holder, per institution. You can verify a bank’s insurance status using the FDIC’s BankFind Suite.

Baselane insures up to $3M¹ on funds deposited via Thread Bank; Member FDIC.

5. Automate rent collection

Manual rent collection is time-consuming and unreliable. Look for fee-free bank accounts with built-in rent collection via ACH or card. Ideally, tenants can set up auto-pay to help reduce late payments, eliminate manual follow-ups, and improve your cash flow.

Avoid monthly fees & minimum balance requirements with Baselane banking

Traditional banks come with a laundry list of account fees, balance requirements, and transaction limits. These charges might seem small at first, but over time, they eat into your cash flow and ROI.

With Baselane, you can connect all your external bank accounts and open unlimited free sub-accounts for multiple entities without monthly fees or minimum balance requirements. Plus, rent collection and bookkeeping are all built in and fully automated, so you can manage your finances without logging into multiple platforms.

Ready for a banking platform that can save you 150 hours and $5,000 per year? Get started for free today.

FAQs

The best bank account for a rental property is a no-fee business transaction account with no monthly fees, unlimited transactions, and tools built for property management. Look for accounts that allow sub-accounts and easy integration with accounting software. Baselane offers all this in one integrated platform built for rental property management.

Yes, having a separate bank account helps you keep track of your rental income and expenses. It also simplifies tax reporting and protects your finances. You can open individual accounts or sub-accounts for each property to stay organized. This is especially important when managing security deposits, as some states require separate accounts or dedicated escrow accounts. Learn more about how to open an escrow account.

Using a business account offers better separation of finances, cleaner bookkeeping, and added legal protection. It’s also the preferred option if you operate under an LLC or have multiple properties.

A landlord-friendly bank account should help you save time and stay organized. Choose an account with no monthly fees, no minimum balance requirements, and free ACH transfers. Look for tools like automated rent collection, sub-accounts by property, and built-in bookkeeping.

Start by choosing a bank account with transparent pricing, no monthly fees, no minimum balance requirements, and no transaction limits. Avoid accounts that only waive fees if you meet conditions like high balances or direct deposits.

Use Baselane to skip monthly fees and other common banking charges, so you can keep more of your hard-earned rental income.

Landlords can save anywhere from $360 to over $3,000 annually by avoiding fees for maintenance, overdrafts, transactions, and minimum balances. These savings add up fast, especially if you manage multiple accounts or LLCs. Switching to a no-fee option is one of the easiest ways to cut operating costs.

Don't miss these

Why Landlords Need a Separate Bank Account for Rental Property

Although not mandatory in all states, creating a separate bank account for rental property transactions can simplify your finances and make tax time much e...

12 December 2023

How to Open an Escrow Account for Security Deposits: A Step-by-Step Guide

Escrow accounts for security deposits offer protection and peace of mind for both landlords and tenants. It’s a secure way to handle funds, ensuring the ...

20 September 2023

State Security Deposit Interest Rate Rules 2025

Security deposit interest rates and rules vary significantly across the United States. This guide covers everything you need to know about security deposit...

2 April 2025